You know what’s funny? The best money decisions I’ve ever made weren’t when I was sitting down with spreadsheets or reading finance books. They happened when I was calm. Just… calm.

After spending over 15 years in banking, I’ve watched people make all kinds of choices with their money. Some brilliant. Some they’d regret within a week. And the wild part? Intelligence, salary, education—none of that guaranteed good decisions. What mattered was whether their head was clear or cluttered when they chose.

An anxious brain sees threats everywhere. A calm one? It sees possibilities.

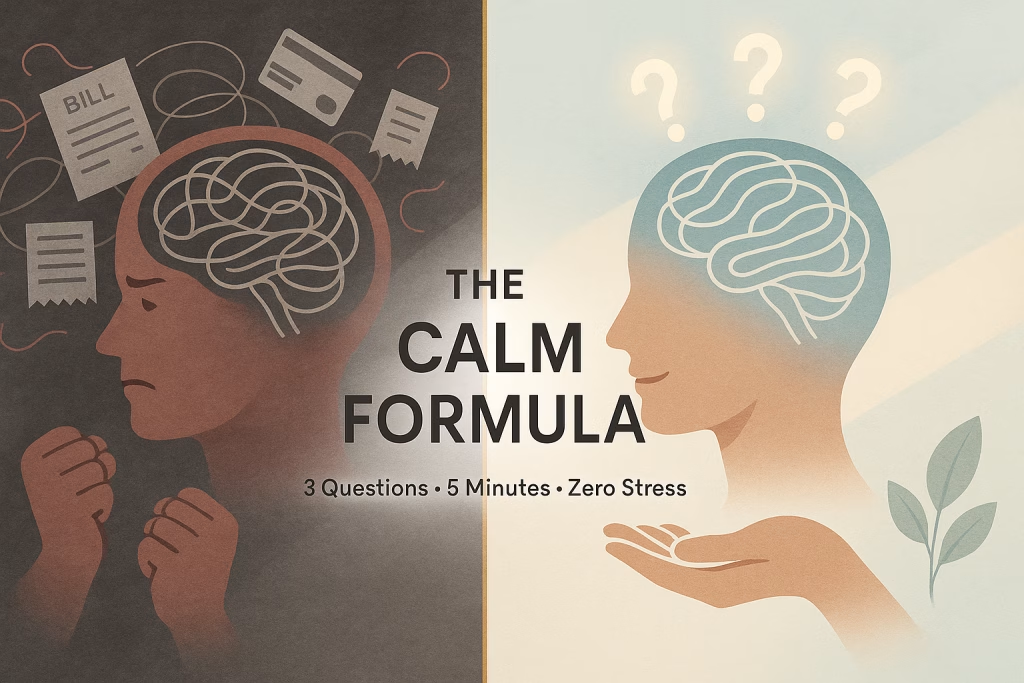

So I’m going to share something I call the calm formula. Three questions that take maybe five minutes—less if you’re in a rush. No fancy financial jargon. No complicated systems. Just a way to think about money that actually reduces stress instead of creating more of it.

Sound too simple? Yeah, I thought so too. Until it worked.

Why Most Money Advice Doesn’t Actually Help

I spent my twenties thinking I was just bad with money.

Read all the right books. Knew about compound interest, emergency funds, that 50-30-20 budgeting rule everyone talks about. Could quote personal finance advice like scripture. But knowing all that stuff? Didn’t change anything. I’d still buy things on impulse and feel sick about it later. Still got that tight feeling in my chest when checking my bank balance.

Turns out, information wasn’t my problem. Overwhelm was.

See, most financial advice treats money like it’s just math. Add this, subtract that, invest here. And sure, numbers matter. But nobody tells you that your relationship with money is about feelings first, logic second. When you’re stressed out, comparing yourself to everyone on Instagram, or just emotionally exhausted—even the smartest financial plan falls apart.

I learned this watching clients at the bank. These were doctors, engineers, successful business owners. Smart people. But they’d make these terrible money choices—not because they were dumb, but because they were fried. Decision fatigue is real, and when your brain is already maxed out, adding financial pressure on top? Forget it.

The calm formula works differently. It starts with how you’re feeling, not what your bank account says. Think of it like clearing fog off your windshield before you drive, instead of just hoping you don’t crash into something.

This isn’t about being perfect or never messing up. It’s about getting clear inside your own head first. When you understand what’s actually happening emotionally, the practical stuff gets way easier. The math starts making sense when the emotions aren’t all tangled up.

Honestly, this changed everything for me. Not just my finances—my sleep got better, my marriage improved, I felt less like I was constantly running from something I couldn’t name. Because here’s the thing: once you figure out how to think calmly about money, that calm leaks into everything else too.

What the Calm Formula Actually Is

Okay, let me just lay it out for you.

Three questions. That’s the whole thing. You ask yourself these every day—morning works best for me, but whenever you remember is fine. Takes five minutes if you really sit with it. Sixty seconds if you’re rushing.

Here they are:

1. What am I actually feeling about money right now?

2. What do I actually need right now versus what I think I need?

3. Does this choice move me toward peace or away from it?

I know. Sounds almost stupidly simple, right? That’s what I thought when I first tried it. But that simplicity is exactly why it works.

Let me tell you about this guy I worked with years ago—I’ll call him Rajesh. Made good money, no huge debts, but constantly stressed about finances. Every expense felt like a mini-crisis. Every bill felt like a personal attack. We sat down one morning over chai, and I just asked him these three questions.

Ten minutes. That’s all it took. He realized his stress wasn’t even about money. It was his dad’s voice in his head—”You’ll never be secure, never be enough”—playing on repeat from childhood. Once he saw that? Everything changed.

The calm formula doesn’t tell you where to invest or how to budget. It gives you something more basic: emotional clarity. And when you’ve got that, all the practical stuff becomes obvious.

I’ve seen this work for college students managing their first real paycheck. Parents juggling three kids and a mortgage. Couples who’d been fighting about money for years. Even wealthy people who realized having more hadn’t made them feel any better.

Because financial peace has nothing to do with the number in your account. It’s about your relationship with whatever number is there.

I use the calm formula every single day now. Before I check my bank balance. Before buying anything over a couple thousand rupees. Before money conversations with my wife, Taniya. It’s become automatic, like brushing my teeth. And just as necessary.

Step 1 – The Awareness Question: “What Am I Actually Feeling About Money Right Now?”

This first question seems obvious, but trust me—it’s not.

Most of us have no clue what we’re actually feeling about money. We just know something feels… off. Tight chest. That heavy feeling. A vague dread when the credit card bill arrives.

About five years ago, I was going to buy a car. Had been wanting it for months. Had the money saved. Made total practical sense. But something felt weird, and I couldn’t figure out what.

So I sat there and asked myself: What am I actually feeling about money right now?

At first? Nothing. Blank. Then slowly, stuff started coming up. Anxiety. My stomach was tight. This weird shame, like I was doing something wrong. And underneath everything? Fear. This irrational terror that if I spent this money, something bad would happen and I’d regret it.

None of this made sense logically. I had savings. Stable job. But the feeling was real, and it was running the whole show without me realizing it.

Emotional spending happens when we ignore what we’re feeling. We shop to feel better. We save obsessively trying to feel safe. We avoid looking at our finances because looking feels too scary. It’s never really about money—it’s about emotions we haven’t dealt with.

Here’s what I’ve figured out: your body knows before your brain does. When you’re about to make a money choice that doesn’t feel right deep down, your body sends signals. Shoulders tense up. Stomach knots. You get restless or distracted for no reason.

The trick is noticing these things without judging them. You’re not trying to fix anything yet. Just naming what’s there.

Try it right now. Close your eyes for a second and think about your money situation. What comes up? Anxiety? Relief? Excitement? Guilt? Nothing at all? Whatever it is—that’s just information.

I’ve had clients realize their financial stress was actually grief over a job loss from years back. Or anger at a partner who didn’t pull their weight financially. Or comparison anxiety from seeing friends’ vacation photos online. The feeling about money is almost never just about money.

Once you know what you’re feeling, you get a choice. Let that emotion make your decisions unconsciously, or acknowledge it and choose consciously anyway.

That morning with the car? Once I recognized the fear, I could ask myself if it was useful. It wasn’t. Just old programming, not current reality. I bought the car, felt good about it, never looked back.

The calm formula starts with awareness because you can’t make a clear decision if you don’t know what’s happening inside. This first question is your check-in, your “Hey, what’s really going on here?”

And sometimes just asking the question shifts everything.

Step 2 – The Clarity Question: “What Do I Actually Need Right Now vs. What Do I Think I Need?”

This second step is where things get uncomfortable. In a good way, but still.

Most of us are terrible at knowing the difference between what we actually need and what we’ve convinced ourselves we need.

I learned this about seven years ago. Working crazy hours at the bank, totally burned out, and I kept buying stuff online. Small things mostly—books I never opened, gadgets I used once, clothes I didn’t even really like. Nothing huge individually, but it added up fast.

One night, Taniya asked me straight up: “What are you actually looking for when you buy all this stuff?”

Got defensive at first. Classic. But then I sat with the question. And it hit me—I wasn’t looking for things. I was looking for relief. From exhaustion. From feeling like my life was just work-sleep-repeat. Those purchases were tiny hits of excitement in an otherwise grey routine.

Once I saw that, I realized I was solving the wrong problem. What I actually needed wasn’t more stuff. It was rest. Time off. A different way of working.

This is where the calm formula gets practical. This second question forces you to separate wants from needs, which is way harder than it sounds.

Here’s how I think about it: short-term relief versus long-term peace. Most impulse decisions give you short-term relief but cost you long-term peace. New phone feels amazing for a week, then it’s just a phone. Expensive dinner feels indulgent in the moment, but if it strains your budget? Creates stress for weeks.

Real needs move you toward long-term peace. They solve actual problems. Line up with what matters to you. Don’t leave you feeling guilty or regretful.

I teach couples to try the “48-hour pause” for big purchases. Want something? Wait two days before buying. During that time, ask yourself: What do I actually need right now?

Sometimes the answer is yes, you genuinely need it. Cool, buy it with confidence.

But usually? The answer is something like, “I need to feel valued” or “I need to prove I’m successful” or “I need to escape my current stress.” And once you know that, you can address the real need instead of just throwing money at the symptom.

There was this couple I worked with—let’s call them Priya and Arjun. Constant arguments about money. Priya wanted a bigger apartment. Arjun wanted to save more aggressively.

When we worked through the calm formula, specifically this second question, something clicked. What Priya actually needed wasn’t more space—it was recognition for everything she did at home, which felt invisible. What Arjun actually needed wasn’t more savings—it was security, because he grew up watching his father struggle financially.

Once they saw what they actually needed—validation for her, security for him—they could address those needs directly. Their money conversations got so much easier after that.

This step is about financial clarity at the deepest level. Seeing past the surface desire to the real human need underneath. When you do that, money decisions become simpler, clearer, way less stressful.

Because you’re not confused anymore about what you’re trying to accomplish. You’re not buying peace at a store when what you really need is a conversation, a boundary, or honestly just a good night’s sleep.

Step 3 – The Direction Question: “Does This Choice Move Me Toward or Away From Peace?”

This third question changed everything for me.

Most financial advice tells you to ask “Can I afford this?” or “Does this fit my budget?” Fine questions, sure. But they miss something crucial. They don’t ask where this choice is taking you emotionally.

Real example from my life: Three years ago, I had a chance to take on more responsibility at work. More money, better title, all the stuff you’re “supposed” to want. On paper, obvious yes.

But when I applied the calm formula, specifically this third question—Does this move me toward peace or away from it?—the answer was crystal clear. Away. Far away.

The role meant longer hours, more stress, less time with my family. And I was already stretched thin. The extra money wouldn’t buy back the peace I’d lose.

So I said no. One of the best decisions I’ve ever made.

The calm formula taught me that financial peace matters more than financial gain when that gain costs you your mental health. This isn’t about being lazy or unambitious—it’s about knowing what you actually want from life.

Here’s how I use this question practically: imagine yourself six months from now. You’ve made this purchase, taken this job, spent this money. How do you feel? Lighter or heavier? More free or more trapped? More yourself or less?

If the answer is heavier, trapped, less yourself—that’s your sign. That choice moves you away from peace, no matter how logical it looks on paper.

Peaceful money decisions have a few things in common. They feel aligned with what matters to you. You don’t have to keep justifying them to yourself. They don’t create resentment. And they usually get easier over time, not harder.

One of my favorite ways to use this question: the “regret test.” I ask myself: If I make this choice, will it haunt me or help me sleep better?

Sometimes the peaceful choice requires short-term discomfort. Saying no to that job meant less money in the short term. Choosing to save instead of splurge means waiting. But here’s what I’ve learned—temporary discomfort in service of long-term peace always feels better than temporary pleasure followed by lasting regret.

I worked with a woman—I’ll call her Meera—who described herself as stuck in a “golden cage.” High-paying job she hated, expensive lifestyle that required keeping that job, no way out that she could see. When we worked through the calm formula, she realized every financial choice she made—the car, the fancy apartment, the vacations—was moving her away from peace.

She made a radical choice. Downsized everything. Smaller place, sold the car, completely changed her lifestyle. Took two years, but eventually she left that job and started something she actually cared about.

Last time I heard from her, she was making about 40% of what she used to. Said she’d never been happier. Because her choices finally moved her toward peace, not away from it.

This third question is your compass. When you’re confused, when practical and emotional pull in different directions, ask yourself: Does this move me toward peace or away from it?

Your gut already knows the answer. You just have to listen.

How to Actually Use the Calm Formula Daily

Alright, so you get the calm formula. Now let’s talk about actually doing it, because knowing and doing are completely different things.

Here’s what works for me: I do it in the morning.

Every morning, before checking my phone or looking at news, I spend five minutes with the calm formula. Sometimes I write in a journal. Sometimes I just sit quietly with coffee. But I ask myself those three questions:

- What am I feeling about money today?

- What do I actually need?

- Am I moving toward peace or away from it?

Some mornings the answers are simple. “Feeling calm. Don’t need anything special. On the right track.” Other mornings there’s more going on. Anxious about an upcoming expense. Tempted by something I saw online. Stressed about a conversation I need to have.

The key is consistency, not perfection. I’ve skipped plenty of days. Life happens, routines fall apart. But every time I come back to the calm formula, it’s like finding solid ground again.

Practical tip: use your phone to help instead of hurt. I have a daily reminder at 7 AM that just says “Calm Formula.” Two words. When I see it, I know what to do. Some people use journal apps, some use voice notes, some just think through it during their morning chai.

Best time to use the calm formula is before major purchases. And I mean before, not while standing at the checkout counter trying to decide. Give yourself space to think. My personal rule: anything over ₹5,000 requires going through all three questions first, ideally the night before.

This has saved me so much money and regret. There was this expensive online course I almost bought last year—something about advanced financial certifications. Sounded impressive. Would’ve cost nearly ₹80,000. But when I sat with the calm formula, I realized I didn’t actually want the certification. I wanted to feel like I was making progress in my career. Two completely different things.

Instead of buying the course, I had an honest conversation with my boss about growth opportunities. Solved the real problem without wasting the money.

Money mindset transformation happens in these small daily moments. Not in one dramatic decision, but in a hundred little ones.

For couples, I recommend using the calm formula together for big financial stuff. Make it a ritual. Sit down with chai, turn off phones, go through the questions together. What are we both feeling? What do we actually need as a family? Does this move us toward the life we want?

This has transformed money conversations for couples in ways that budgets and spreadsheets never could. Because it’s not about controlling each other—it’s about understanding each other.

When you skip a day, or a week, or a month: just start again. No guilt. The calm formula isn’t about perfection. It’s about creating moments of clarity whenever you can.

Even if you only use it once a week, or only before major decisions, it’ll still change your relationship with money. Because it rewires how you think. Shifts you from reactive to reflective. From anxious to aware.

What Actually Changes When You Think This Way

I’m not going to lie and say the calm formula will make you rich or solve everything overnight. That would be BS.

But I can tell you what actually changes, because I’ve lived it and watched dozens of clients live it too.

First: reduced impulse spending. Not because you’re white-knuckling through temptation, but because the impulse itself gets weaker. When you’re checking in with your emotions daily, you catch yourself earlier. You notice the urge to buy something before you’ve already bought it.

I used to be awful with impulse purchases. Online shopping at midnight, grabbing stuff I didn’t need because it was “on sale.” Now? Still get tempted sometimes, but there’s a pause. A little voice that asks: What am I actually feeling? What do I actually need? Usually that pause is enough.

Second: better sleep. Seriously. Financial anxiety wrecks sleep. When you’re not constantly worrying about money, or feeling guilty about past choices, or stressed about future ones—you sleep better. Your whole nervous system relaxes.

Someone told me once that financial peace isn’t about having a certain amount. It’s about not thinking about money all the time. That’s exactly what the calm formula does. Helps you think about money clearly when you need to, then let it go the rest of the time.

Third: relationship improvements. If you’re in a relationship, money is probably one of your top sources of conflict. When both people start using the calm formula, something shifts. You stop fighting about surface stuff—who spent what, who forgot which bill—and start addressing real issues underneath.

Taniya and I had this recurring fight about groceries. She’d buy organic everything, I’d complain about the cost. Round and round. When we finally applied the calm formula to it, we discovered the real issue: I felt like my opinion didn’t matter in household decisions, she felt like I didn’t trust her judgment. Once we addressed that, the grocery thing resolved itself.

Calm money thinking also leads to more confident decision-making. When you’re checking in with yourself regularly, you start trusting your gut more. Not second-guessing every choice or constantly wondering if you made the right call. You make a decision, know why you made it, move on.

There’s also this side effect: natural shift toward simplicity. The more you practice the calm formula, the more you realize how little you actually need to be happy. Start questioning automatic upgrades, keeping-up-with-others purchases, stuff that clutters your life without adding value.

Not talking about becoming some extreme minimalist—though if that’s your thing, cool. Just naturally gravitating toward what actually matters to you. Less noise, more signal.

And maybe most important: long-term wealth building gets easier. Not because of some complex investment strategy, but because you stop sabotaging yourself. Not stress-spending away your savings. Not making fear-based decisions that cost money. Thinking clearly, acting intentionally, and that consistency compounds.

I’ve watched clients double their savings without feeling deprived. Build investment portfolios that actually match their risk tolerance. Start businesses they’d dreamed about for years. None of this from fancy financial tricks—just calm, clear thinking about money.

Common Obstacles (And How to Handle Them)

Let’s be real—the calm formula sounds great in theory, but actually doing it? That’s where people get stuck.

So let me hit the obstacles I hear most often, and how to work through them.

“I don’t have time for daily reflection.”

Yeah, I hear this a lot. You’re busy, I’m busy, everyone’s busy. But here’s the thing: the calm formula takes as much time as scrolling Instagram for five minutes. We all have the time—we’re just choosing to spend it elsewhere.

If five minutes feels impossible, try sixty seconds. Quick check: How am I feeling about money? Good? Stressed? What do I need today? Done. Even that tiny pause creates more financial clarity than going through your day on autopilot.

“My situation is too urgent for calm thinking.”

Heard this from people drowning in debt, facing job loss, dealing with medical emergencies. When crisis hits, calm feels impossible.

But here’s what I learned: calm money thinking matters most during crisis, not least. Panic makes bad situations worse. When you’re in crisis mode, even two minutes of the calm formula can shift you from reactive to responsive. Not perfectly, not all at once, but enough to make your next decision slightly better.

One client was facing bankruptcy. Completely overwhelming. But we used the calm formula anyway, one small decision at a time. What needs addressing first? What moves toward stability, even a tiny bit? Those small calm moments added up to a complete turnaround over eighteen months.

“This feels too simple to work.”

Our brains think complicated problems need complicated solutions. So when something as simple as three questions shows up, we dismiss it.

But complexity is often just confusion dressed up. The most powerful tools—breathing, listening, noticing—are simple. They work not despite simplicity, but because of it.

Try it for one week. Just seven days. If it doesn’t help, you’ve lost nothing. But I’m betting you’ll notice something shift.

“When emotions feel overwhelming.”

Sometimes you ask “What am I feeling about money?” and the answer is: Everything. All at once. Too much.

When that happens, don’t try sorting through it all. Just name the loudest feeling. Maybe it’s fear. Okay, fear. That’s enough. You don’t need to analyze where it came from or fix it right now. Just acknowledging it takes away some power.

And honestly, if your financial stress is consistently overwhelming, that might mean you need more support than a daily practice can provide. Therapy, financial counseling, trusted friends—no shame in getting help.

“My partner thinks this is silly.”

Not everyone’s going to get the calm formula right away. That’s okay. Practice it yourself first. Let your changes speak for themselves.

When your partner sees you making clearer decisions, feeling less stressed, sleeping better—they’ll get curious. Maybe then you introduce it. Or maybe they find their own version.

But you don’t need permission to think clearly about money. Start with you.

“The comparison trap won’t let me be calm.”

Social media is designed to make you feel behind. Your colleague bought a new car, your friend went on an amazing vacation, your cousin bought a house. Suddenly your calm money life feels… boring? Insufficient?

What helps me: unfollow or mute anyone who makes you feel bad about your financial situation. Sounds harsh, but your mental health matters more than their content.

And remember—you’re seeing everyone’s highlight reel, not their bank statements, stress levels, or credit card debt. Financial peace isn’t about keeping up. It’s about knowing what’s enough for you.

“How do I maintain this during stress?”

Life happens. Jobs get stressful, kids get sick, parents need care, relationships hit rough patches. During those times, the calm formula might slip.

That’s human. Don’t beat yourself up. Just come back when you can. Even if you only remember one question—usually that third one: Does this move me toward peace?—that’s enough to guide you through rough times.

The practice isn’t about perfection. It’s about having a tool you can return to whenever you need it.

Beyond the Formula: Building a Calm Money Life

The calm formula is a daily practice, but it’s also a gateway to something bigger—an entirely different way of relating to money and life.

Once you start thinking clearly about money, you notice how much of modern life is designed to keep you confused, anxious, constantly wanting more. And you start making choices to protect your calm money life from that noise.

Creating a calm money environment matters more than people realize. Look around your space right now. Stacks of unopened bills? Credit cards you don’t use? Bank statements you’re afraid to read? Physical clutter creates mental clutter.

I spent one weekend about two years ago completely reorganizing my financial life. Closed unnecessary accounts. Unsubscribed from promotional emails. Set up automatic payments for recurring bills. Created one simple folder for important documents. Nothing fancy, just basic organization.

Mental relief was immediate. When your money environment is calm, thinking about money becomes calmer too.

The role of learning can’t be ignored either. The more you understand about how money actually works—not get-rich-quick schemes, but real financial principles—the more confident you become.

Not talking about becoming a financial expert. Just understanding basics like how compound interest works, what different investment options mean, why insurance matters. Knowledge reduces fear. Less fear means more financial clarity.

Some books that helped me: The Psychology of Money by Morgan Housel, Your Money or Your Life by Vicki Robin. Even simple explainer videos on YouTube about financial concepts. You don’t need to go back to school—just be curious and willing to learn.

When to seek professional help is important too. The calm formula is powerful, but it’s not therapy and it’s not financial planning. If you have serious debt, complex investment questions, or deep emotional issues around money, get professional support.

Good financial advisor helps with technical stuff. Good therapist helps with emotional stuff. The calm formula works alongside both, helping you stay grounded while doing harder work.

Building community around calm money has been surprisingly important for me. When everyone around you is chasing the next big thing, comparing salaries, stressing about status symbols—hard to stay calm.

Find your people. Maybe online communities focused on financial wellness. Maybe friends who share your values. Maybe family members who get it. You need at least a few people who understand that peace matters more than appearances.

I’ve got a small group of friends who meet quarterly to talk about money openly. No judgment, no competition, just honest conversations about what we’re learning, where we’re struggling, what’s working. Those conversations have taught me more than any book.

Next level practices emerge naturally once you’ve used the calm formula for a while. You might start tracking not just spending, but emotional patterns around spending. Might create rituals around big financial decisions. Might develop your own questions that go even deeper.

For me, I added a monthly review where I look back at the past thirty days and ask: What money decisions did I make? Which brought peace? Which brought stress? What pattern am I noticing?

This reflection helps me learn from my own experience, which is way more powerful than learning from generic advice.

And this is exactly why Taniya and I started The Passive Rich. Because we believe in calm money thinking, in financial peace, in building a life that feels rich from the inside.

Our upcoming book, The Five Gates of Wealth, releases February 21st, 2026. It’s a story about a couple navigating money decisions, relationship challenges, the invisible work of building a meaningful life. Everything I’ve shared here—the calm formula, the emotional side of money, the journey toward peace—is woven throughout that story.

If this resonated with you, the book will too. For people tired of financial advice that ignores emotional reality. For people who want less stress and more clarity. For people ready to build a calm money life, one honest choice at a time.

Conclusion

Money will always be part of life. Financial stress? That’s optional.

The calm formula isn’t magic. Just three honest questions you ask yourself every day. Questions that help you notice what you’re feeling, clarify what you actually need, choose what brings peace instead of pressure.

I’ve seen this simple practice transform how people relate to money. Not overnight. Not dramatically. But steadily, quietly, deeply.

First question—What am I feeling about money?—creates awareness. Second question—What do I actually need?—creates clarity. Third question—Does this move me toward peace?—creates direction.

Together, these questions form a daily money mindset practice that reduces financial stress, improves decision-making, builds genuine wealth of the mind.

Start tomorrow morning. Ask yourself those three questions. See what shifts.

You don’t need to overhaul your entire financial life in one day. Just start thinking clearly, one day at a time. That’s how calm money thinking becomes a way of life. That’s how financial peace becomes real, not some distant goal.

And if you’d like these ideas in your inbox every week—stories, lessons, occasional hard truths—join The Calm Letter. Free, weekly, written for people who want less noise and more clarity.

Subscribe to The Calm Letter

Because the richest life isn’t the one with most money. It’s the one with most peace.

You can start building that today. Three simple questions. A willingness to think clearly about what you actually want from money—and from life itself.

The calm formula is waiting. All you have to do is ask.